If you’re shopping for a home on Oahu, you’ve probably already noticed that three little letters keep popping up in every listing: HOA. And right next to them, a monthly number that ranges from surprisingly low to “wait, is that a second mortgage?”

Oahu HOA fees are one of the most misunderstood costs in Hawaii real estate. Some buyers write off entire property types because the fees seem too high. Others ignore them completely and get blindsided when they realize how much those fees affect their monthly budget and mortgage qualification.

I’m Devin Hammack with Island Home Oahu at eXp Realty, and I walk buyers through this conversation every single week. This guide is everything I wish someone had handed me when I first moved to Oahu after leaving the Navy. No fluff, no sales pitch. Just real numbers and honest advice so you can make a smart decision.

[Image: Aerial view of Oahu condo buildings along the coast. Alt text: “Condo buildings on Oahu where HOA fees vary widely by property type and location”]

What Do HOA Fees on Oahu Actually Cover?

Before we talk numbers, let’s talk about what you’re actually paying for. An HOA fee isn’t just some arbitrary charge that a building slaps on top of your mortgage. It covers real expenses that keep your property functioning and (ideally) appreciating in value.

Here’s what most Oahu HOA fees include:

Common Area Maintenance: This is the big one. Think landscaping, hallway lighting, elevator maintenance, pool upkeep, lobby cleaning, parking structure repairs, and exterior building maintenance. In a high rise, this gets expensive fast because there’s a lot of shared infrastructure.

Building Insurance: Your HOA carries a master insurance policy on the building’s structure and common areas. This is separate from your individual condo insurance (called an HO-6 policy), which covers the interior of your unit and your personal belongings. In today’s market, this line item is the fastest growing part of most Oahu HOA budgets, and I’ll explain why below.

Reserve Fund Contributions: A portion of every monthly fee goes into a reserve fund. This is money set aside for major future repairs like roof replacements, elevator overhauls, plumbing upgrades, and exterior repainting. A healthy reserve fund is one of the most important things you’ll evaluate as a buyer.

Utilities (Sometimes): Depending on the building, your HOA fee might include water, sewer, trash, cable TV, or even internet. Some older buildings include all utilities. Some newer ones include almost none. This matters a lot when comparing fees between properties.

Amenities: If your building has a gym, pool, BBQ area, recreation room, security, or concierge service, those operating costs come out of your HOA fees.

Management Company Fees: Most associations hire a professional management company to handle day to day operations, accounting, and vendor coordination. That cost is baked into your monthly fee.

[Image: Condo pool and amenity area in Kakaako. Alt text: “Pool and common area amenities covered by Oahu HOA fees in a Kakaako condo”]

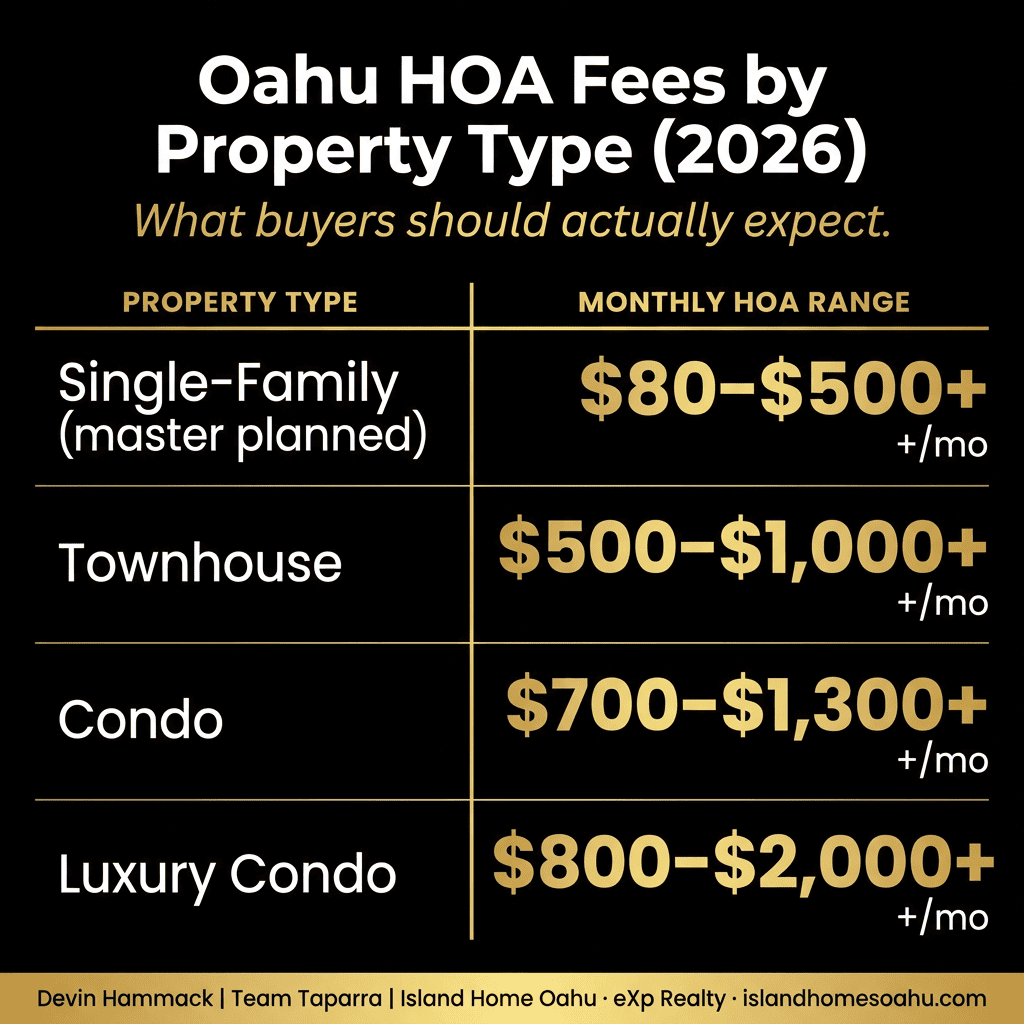

Average Oahu HOA Fee Ranges by Property Type

This is the question everyone asks first: “How much are HOA fees on Oahu?” The honest answer is that it depends entirely on the property type, the building’s age, and what’s included. But here are realistic ranges based on what I see in the market right now.

Low-Rise Condos (Walk-Ups, 3 to 6 Stories)

Typical range: $300 to $600 per month

These buildings are generally simpler. No elevators (or just one), smaller common areas, and fewer amenities. You’ll find a lot of these in neighborhoods like Kailua, Kaneohe, Pearl City, and parts of town outside of the Kakaako/Waikiki core. Fees tend to be more predictable because the infrastructure is less complex.

High-Rise Condos

Typical range: $500 to $1,200+ per month

High rises have elevators, fire suppression systems, parking garages, security, and larger common areas. All of that costs money to maintain. Buildings in Kakaako, Waikiki, and Ala Moana typically fall in this range. Newer buildings sometimes have lower fees initially, but expect them to rise as the building ages and maintenance needs increase.

Luxury Condos

Typical range: $800 to $2,000+ per month

Buildings like Park Lane, Waiea, Anaha, and Hokua offer premium amenities: concierge service, valet parking, resort style pools, private dining rooms, and high end fitness centers. You’re paying for a lifestyle, and the fees reflect that. Some luxury buildings in Ward Village and Kakaako push well past $1,500 per month for larger units.

Townhouses

Typical range: $200 to $500 per month

Townhouse communities generally have lower fees because there’s less shared infrastructure. You might share exterior maintenance, landscaping, a community pool, and common area insurance, but you’re responsible for more of your own property compared to a condo. Areas like Ewa Beach, Mililani, and Hawaii Kai have a lot of townhouse communities in this range.

CPR (Condominium Property Regime) and Detached Condos

Typical range: $90 to $250 per month, sometimes higher in amenity-rich communities

This one surprises a lot of buyers. Communities like Ho’opili in Ewa Beach are technically condominiums even though the homes look and live like single family houses. On the simple end, a small CPR with little more than shared landscaping and basic administration can run under $100. But in a large master planned community, you’re often paying two fees stacked together: a neighborhood level CPR maintenance fee plus a master association fee that funds the community’s parks, pools, recreation centers, and trails. In a community like Ho’opili, with multiple pools, parks, a dog park, and miles of trails, those two fees combined can land you in the $150 to $250 range depending on the neighborhood. The more a community offers, the more it costs to maintain, so don’t assume “detached condo” automatically means cheap.

Single-Family Homes in Master Planned Communities

Typical range: $50 to $200 per month

Some single family neighborhoods on Oahu have HOA fees too, especially master planned communities in Kapolei, Ewa Beach, and parts of Central Oahu. These fees are usually modest and cover things like community parks, walking paths, entry monuments, and neighborhood landscaping.

[Image: Comparison chart showing HOA fee ranges by property type. Alt text: “Chart comparing average Oahu HOA fees by property type from CPR homes to luxury condos”]

What’s Included vs. What’s Not

One of the biggest mistakes buyers make is comparing HOA fees without looking at what’s included. A $900 HOA fee that includes water, sewer, cable, internet, and building insurance might actually cost you less out of pocket than a $500 fee that covers almost nothing beyond basic maintenance.

Here’s what to ask about every property:

Water and sewer: Included in the fee, or billed separately? On Oahu, the Board of Water Supply charges can add $50 to $100+ per month depending on usage.

Electricity: Rarely included in HOA fees, but some older buildings do include it. Hawaii has some of the highest electricity rates in the country, so this is worth knowing.

Cable and internet: Some buildings have bulk agreements with providers that bring costs way down. Others leave it entirely up to you.

Parking: Most condos include one stall. Some charge extra for a second stall, and some luxury buildings charge for all parking separately.

Storage: Some buildings include a storage locker. Others charge monthly rent for storage units.

Insurance: Your HOA’s master policy covers the building structure, but you still need your own HO-6 policy for interior coverage and personal liability, and you’ll want loss assessment coverage on that HO-6 (more on why in the insurance section below).

When I’m helping buyers compare properties, I always build a total monthly cost worksheet that factors in all of these items. Two condos with a $300 difference in HOA fees might end up costing nearly the same when you account for included utilities. If you want the full financial picture of island life, my cost of living on Oahu guide breaks down the rest.

How to Read HOA Financial Documents

This is where most buyers glaze over, and I get it. Financial documents aren’t exciting. But spending 30 minutes reviewing them can save you tens of thousands of dollars. Here are the three documents you need to look at.

The Reserve Study

A reserve study is a professional assessment of the building’s major components (roof, elevators, plumbing, exterior paint, parking structure, etc.), their expected lifespan, and how much money the association needs to save to replace or repair them. A well funded reserve is generally considered to be at 70% or above. Below 50% is a concern. Below 30% is a serious red flag.

Hawaii requires associations to conduct reserve studies, and the results should be available to you during your due diligence period. Ask for the most recent one. For more on your rights and the rules associations operate under, the Hawaii Real Estate Commission publishes helpful condominium resources.

The Annual Budget

The budget tells you exactly where your monthly fee goes. Look at the line items. How much goes to management fees? Maintenance? Insurance? Reserves? If the reserve contribution is suspiciously low, that’s a sign the board might be keeping fees artificially low at the expense of long term building health.

Meeting Minutes

Board meeting minutes from the past 12 to 24 months will tell you about upcoming projects, owner complaints, pending lawsuits, insurance claims, and general building drama. Yes, building drama. You want to know if there’s an ongoing feud between the board and owners, or if there’s a major repair being debated that could lead to a special assessment.

Red Flags to Watch for in an HOA

Not all HOA fees are created equal. A low fee isn’t always a good sign, and a high fee isn’t always a bad one. Here’s what should make you pause and dig deeper.

Special Assessments

A special assessment is a one time charge that the HOA levies on all owners to cover a major expense that the reserve fund can’t handle. Think $10,000 to $50,000+ per unit for things like concrete spalling repairs, full building repainting, or elevator replacements. Special assessments happen when reserves are underfunded, or when an insurance bill comes in far higher than anyone budgeted for. Before you buy, ask if there are any current or pending special assessments.

Underfunded Reserves

If the reserve study shows the fund is below 50%, that building is at higher risk for special assessments down the road. Some buildings keep fees low by underfunding reserves, and owners pay the price later.

Pending Litigation

Lawsuits against the HOA (or by the HOA against a developer or contractor) can be expensive and can affect the building’s insurability. Your lender may also have issues with this.

Deferred Maintenance

If you tour a building and the hallways look tired, the elevators break down frequently, or the parking garage has visible concrete damage, those are signs that maintenance has been deferred. That deferred maintenance will eventually become an expensive repair, likely funded by higher fees or a special assessment.

Rapid Fee Increases

Ask for a history of HOA fee changes over the past five years. Modest annual increases of 3% to 5% are normal. Jumps of 15% to 20% year over year suggest the building is catching up on deferred costs, or absorbing a big insurance increase. For more on well run associations versus troubled ones, the Community Associations Institute, Hawaii Chapter is a solid resource.

The Insurance Factor: Why Many Oahu HOA Fees Are Climbing

If you’ve heard that Oahu HOA fees are rising fast, insurance is the single biggest reason why. Hawaii has been working through a condo insurance crisis, and it lands directly on maintenance fees and special assessments across the island. This is the most important section in this guide for anyone buying a condo or CPR home right now.

Here’s the short version. Master hurricane and property insurance premiums for many Oahu buildings have climbed dramatically over the past couple of years, with some associations seeing renewals jump several hundred percent at once. As insurers pulled back or declined to renew, boards were pushed onto the expensive surplus lines market just to keep coverage in place. Someone has to pay those premiums, and that someone is the owners, through higher monthly fees or one time special assessments.

It gets more serious than cost alone. A large number of Oahu associations have chosen to carry less than 100% replacement coverage on their master policies because full coverage became unaffordable. That matters to you as a buyer for two reasons. First, if a disaster hits, an underinsured building may not have enough money to rebuild. Second, and more immediately, many lenders will not finance a unit in an underinsured building. I have seen buyers get well into escrow only to have financing collapse because the building’s master policy didn’t meet the lender’s requirements. If you’re using a VA or conventional loan, this is not a hypothetical.

The state stepped in with Act 296 in 2025, which reactivated the Hawaii Hurricane Relief Fund for associations that can’t find coverage on the private market and created a loan program to help buildings fund the repairs that make them insurable again. It’s meaningful relief, but it hasn’t erased the problem, and premiums remain elevated.

What this means for you as a buyer:

- Ask for the building’s current master policy and certificate of insurance, and confirm it carries 100% replacement cost coverage, including hurricane.

- Ask your lender early whether the building meets their insurance requirements, before you’re emotionally attached to a specific unit.

- Carry loss assessment coverage on your own HO-6 policy. This is the coverage that steps in if the association levies a special assessment to cover an insurance shortfall or a large deductible. It’s inexpensive, and in today’s market it’s essential.

You can read more through the state’s condominium insurance resources. And if you want me to review a specific building’s insurance situation before you write an offer, that’s exactly the kind of thing I do for my buyers.

How Oahu HOA Fees Affect Your Mortgage Qualification

Here’s something that catches a lot of first time buyers off guard. Your lender doesn’t just look at your mortgage payment when calculating how much you can afford. They include property taxes, homeowner’s insurance, and your monthly HOA fee in your debt to income (DTI) ratio.

That means a $700 HOA fee effectively reduces the mortgage amount you qualify for. On Oahu, where home prices are already high, this can make a real difference in what you can afford.

Let me put it in practical terms. If your target total monthly housing payment is $4,000, and the HOA fee is $800, you only have $3,200 left for principal, interest, taxes, and insurance. That’s a significant reduction in buying power.

If you’re using a VA loan (which many buyers on Oahu are, given our large military community), the VA also requires that the condo project be on the VA approved list. Not all buildings qualify, and high HOA fees combined with special assessments or insurance shortfalls can affect a building’s VA approval status. My VA loan home buying guide for Oahu walks through the full process. And if you’re still weighing whether ownership makes sense at all, my renting vs. buying on Oahu breakdown runs the numbers.

Leasehold vs. Fee Simple: How It Connects to HOA Fees

Hawaii is one of the only states where leasehold property is common, and it directly affects your cost analysis when evaluating Oahu HOA fees.

With fee simple ownership, you own the land under your unit (or your share of the land in a condo). With leasehold, you own the building or unit, but you lease the land from a landowner (often a trust or estate). Leasehold properties typically have an additional monthly lease rent on top of your HOA fee.

So if you see a condo with a low sale price and reasonable HOA fee, check whether it’s leasehold. That extra $300 to $800 per month in lease rent changes the entire equation. Some leasehold properties have converted or are in the process of converting to fee simple, which eliminates the lease rent but may result in a higher purchase price.

Always factor lease rent into your total monthly housing cost alongside the HOA fee. If you’re deciding between a condo and a house in the first place, my single-family home vs. condo living guide compares the tradeoffs.

AOAO vs. HOA: Hawaii’s Unique Terminology

If you’ve been reading condo documents on Oahu, you’ve probably seen the term AOAO and wondered if it’s different from an HOA. Let me clear this up.

AOAO stands for Association of Apartment Owners. Under Hawaii Revised Statutes Chapter 514B, condominiums are governed by an AOAO, not an HOA. The function is essentially the same. The AOAO manages the common elements, collects maintenance fees, maintains reserves, and enforces house rules.

The term HOA (Homeowners Association) is more commonly used in planned communities, townhouse developments, and CPR properties on Oahu. Functionally, they serve similar purposes, but the legal framework and governing statutes differ slightly.

For practical purposes as a buyer, the distinction mostly matters when you’re reading legal documents. Your real estate agent and attorney can help you understand which structure applies to the property you’re considering.

Frequently Asked Questions About Oahu HOA Fees

Can HOA fees go down?

It’s rare, but it can happen. If a building completes a major project that was driving up costs, or if the association refinances insurance at a lower rate, fees might decrease slightly. But in general, expect HOA fees to increase over time as maintenance costs, insurance premiums, and labor costs rise.

Are HOA fees tax deductible?

For your primary residence, HOA fees are generally not tax deductible. If the property is a rental or investment property, HOA fees can typically be deducted as a business expense. Always consult with a tax professional for your specific situation.

What happens if I don’t pay my HOA fees?

The association can place a lien on your property, charge late fees and interest, and eventually foreclose on the lien. In Hawaii, AOAO liens carry a limited “super priority,” meaning a portion of unpaid fees can take priority even over your mortgage. Don’t skip your HOA payments.

Can I negotiate HOA fees when buying?

No. HOA fees are set by the association’s board and apply equally to all owners. You can’t negotiate a lower fee for your unit. What you can do is factor the fee into your purchase offer. If the HOA fee is high, that may justify offering less for the unit itself.

How often do HOA fees increase on Oahu?

Most associations review and adjust fees annually. Typical increases run 3% to 5% per year. Larger increases usually happen when insurance premiums spike (which has been very common in Hawaii recently) or when the building needs to catch up on underfunded reserves.

What to Do Before You Buy

If you’re a first time buyer on Oahu, don’t let HOA fees scare you away from condos entirely. Some of the best values on the island are in well managed condo buildings where the fees are reasonable and the reserves are healthy. My first-time home buyer guide for Oahu covers the whole journey if you’re just getting started.

Here’s my simple checklist:

- Get the total monthly cost picture. Mortgage payment plus taxes plus insurance plus HOA fee plus any lease rent plus utilities not covered by the HOA.

- Read the reserve study. Look for 70%+ funding.

- Review the last two years of meeting minutes. Look for red flags like pending assessments, lawsuits, or major deferred repairs.

- Check the master insurance policy. Confirm 100% replacement coverage and ask your lender if the building qualifies.

- Ask about recent and upcoming fee increases. A stable history is a good sign.

- Compare apples to apples. Factor in what each HOA fee includes before deciding one building is “cheaper” than another.

Let’s Talk About Your Oahu Home Search

Understanding Oahu HOA fees is just one piece of the puzzle, but it’s an important one. The right property at the right price with a well managed HOA can be one of the smartest investments you make on this island.

If you have questions about a specific building, want me to pull the HOA documents on a property you’re considering, or just want to talk through your options, I’m here. No pressure, no obligation, just honest advice and clear communication.